On May 7th, the Central Bank presented the report corresponding to the market expectations survey for the month of April. It includes forecasts from 39 participants regarding the future evolution of the main economic variables.

The REM analysts project a real Gross Domestic Product (GDP) level for 2024 that is 3.5% lower than the average for 2023. The Top-10 participants projected, on average, a 3.7% reduction for the year.

In Argentina, economic recessions are not surprising; it's something we experience periodically and that every Argentine has suffered from to a greater or lesser extent. However, despite being such a recurrent phenomenon, it is not common to have a historical analysis of the product and the way its components vary.

To broaden general knowledge about this phenomenon that negatively affects the quality of life of Argentines, the behavior of the GDP during the period 1920–2023 is evaluated below. Then, briefly, it is analyzed how its components evolved in those years where economic activity declined (as expected in 2024).

GDP Behavior 1920 – 2023

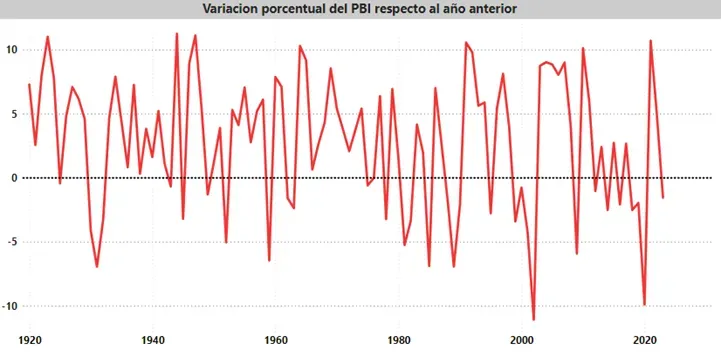

The following graph presents the evolution of the GDP from 1920 to 2023, using annual data expressed in millions of pesos at 2004 prices.

Source: Own elaboration based on Fundación Norte-Sur

The trend from end to end is clearly upward, the product grew 14.5 times between 1920 and 2023. It is also quickly noticeable the economic stagnation that has taken place since 2011, where since then GDP has practically remained constant despite demographic growth.

Another aspect worth highlighting is the instability of the series: out of 104 years analyzed, in only 68% the variation compared to the previous year was positive. The average variation was 2.8%. There were 7 times when the product grew more than 10%, and in 9 cases the activity fell by more than 5%.

Source: Own elaboration based on Fundación Norte-Sur

Public and private consumption

Using the expenditure method, GDP results from the sum of consumption (public and private), investment or FBKF, and net exports.

GDP = CONSUMPTION + INVESTMENT + EXPORTS - IMPORTS

With this in mind, it is interesting to know how each of its components was affected during the recessive years, identifying systematic behavior patterns that can help us when evaluating future scenarios.

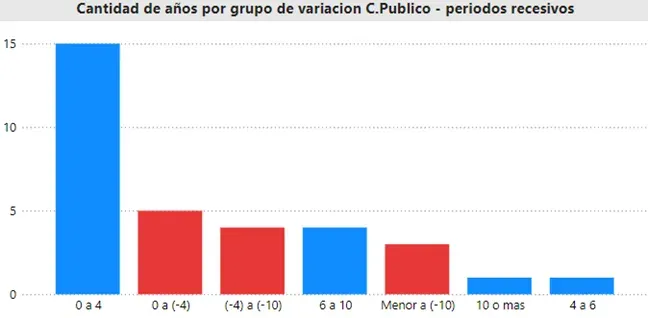

Starting with public consumption, it is observed that it moved in the opposite direction to the product in 21 of the 33 recessive years, of which 6 took place in the last two decades. This reflects, to a large extent, the crowding-out effect that took place from public consumption towards private.

Looking in more detail, it can be seen that despite the unfavorable evolution of economic activity, public sector consumption grew by 9 times to 4% (45% of the recessive period), even growing more than 10% on one occasion and 4 times between 6% and 10%.

Source: Own elaboration based on Fundación Norte-Sur

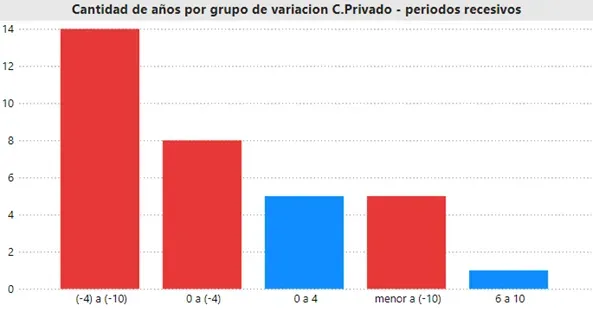

The hypothesis of the crowding-out effect is confirmed when seeing that, out of the 33 recessive years, in only 6 did private consumption increase. In the 27 red years, it contracted between (-4%) and (-10%), while in 5 periods it registered a deterioration greater than (-10%). The situation worsens if we consider that, in the last 23 years, Argentina saw private sector consumption contract compared to the previous year 40% of the time.

Source: Own elaboration based on Fundación Norte-Sur

Investment

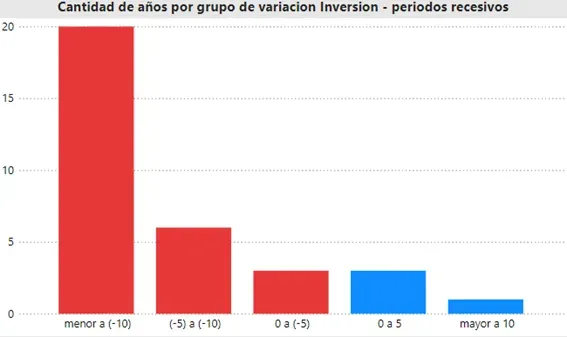

Investment is naturally an intertemporal process that largely depends on the future expectations of the investor. Economic volatility and the decline in the level of activity are detrimental to investment, so it is expected that it will decrease during recessive periods.

As shown in the following graph, out of 33 years in recession, investment fell during 29, which represents 87% of the total time. In addition, when the economy fell by more than 2%, investment always dropped by more than 5%, with a maximum drop of 37% in 2002.

Source: Own elaboration based on Fundación Norte-Sur

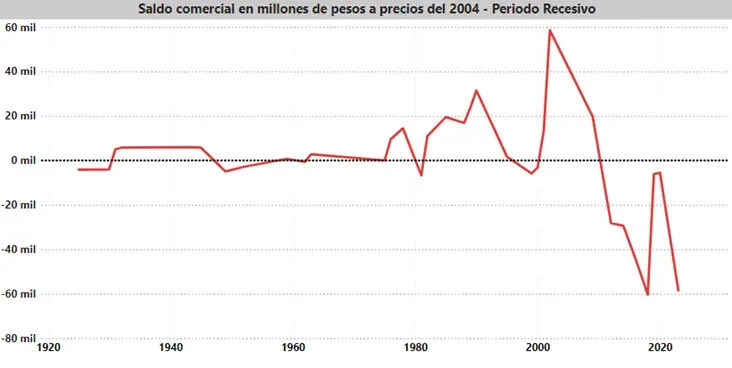

Trade balance

Last but not least, we see how the current account trade balance performed for the same subset of time.

The decline in the activity level and the reduction in citizens' purchasing power leads to a lower demand for imports. In addition, in general, during recessive periods, the exchange rate increases incentivizing exports. Due to these two phenomena, a trade surplus should be observed during the recessionary stage of the cycle.

As shown in the following graphic, the trade balance has been in surplus for 18 periods and in deficit for 15. That is, unlike the previous components, this does not follow a systematic behavior pattern.

Source: Own elaboration based on Fundación Norte-Sur

Filtering by group of GDP variations, it can be seen that when it contracts by more than 2%, the trade balance results in a surplus (14 out of 18 years), while when the decline is less than 2%, imports outstrip exports, leading to a trade deficit.

What should we expect?

History shows us that when the product falls by more than 3%, both private consumption and investment will be reduced by an equal or greater amount. On the other hand, public consumption could either grow or fall; there is no clear trend for it. Lastly, on the external front, we should expect a trade surplus.

This projection is made based on the previously provided historical data; thus, it should be taken as such, as a lesson from the past.

Various reasons can lead us to assume a structural change, a turning point, from the new government's economic policies. By gathering the necessary conditions to energize the productive sector through more and better investments, a more favorable scenario could be achieved. Let's hope the same history does not repeat itself.

Comments