The exchange "peg" is becoming more and more a topic of debate, with many economists stating that without its elimination the country will not be able to return to the path of growth. However, little is developed as to what this concept means, why it is used and how its elimination would have a positive impact on the economy.

In order to provide the non-economics reader with the necessary knowledge on the subject, each of these points is briefly but concisely developed below.

What does the cap imply?

First of all, it should be explained that the "cepo" is nothing more than the official intervention on the foreign exchange market. This economic policy tool implies that the normal supply and demand mechanisms are totally or partially relegated and, in their place, an administrative rule on the purchase and sale of foreign currency is implemented.

The new administrative rule governing control over the official foreign exchange market may impose both qualitative and quantitative restrictions. The control modalities are not always the same, but they are generally applied:

1. restrictions on the purchase of foreign currency either by the public or by companies.

2. Import authorizations

3. Taxes on foreign exchange transactions

4. Controls on the repatriation of capital

5. Differentiated exchange rates

In addition, controls on capital flows regulating the inflow and outflow of portfolio investment, foreign direct investment and other financial investments are often employed.

Why is it used?

In most cases they are used as an instrument to save the external account of the public sector, as a consequence of cash needs. Tacit in this definition is an emergency in the balance of payments, which indicates that, until the crisis and the implementation of controls, the central bank adhered to a more or less fixed parity scheme.

In other words, after the previous adoption of an exchange system that establishes fixed parities between the domestic currency and international currencies, and after repeated negative balances either on the current and/or financial account, which are compensated by a loss of reserves, the central bank runs the risk of no longer being able to comply with the parity it established and ends up implementing the previously mentioned controls.

It is not the fault of the companies or the public that demand foreign currency, whether for commercial or monetary purposes. The control mechanisms arise because the national government does not wish to carry out the exchange rate corrections necessary to eliminate the excess demand, even though history shows that this excess is a consequence of the economic policies previously implemented.

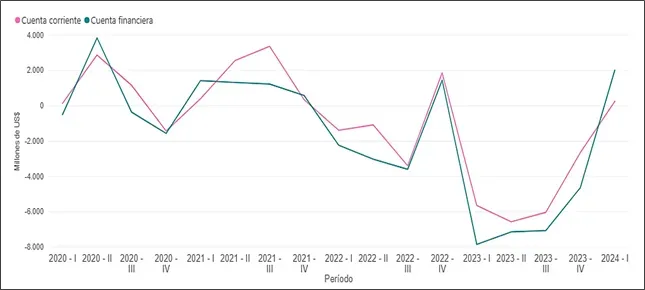

Current and financial account of the balance of payments. In millions of USD

Source: BCRA

What would be the benefits of eliminating controls?

The elimination of exchange controls could have a positive impact on investment and consumption, and therefore on the level of activity and income of the population. That is why so much emphasis is placed on this issue.

The effects on investment are clear: The decision to invest is an intertemporal act, where present resources are made available in order to obtain a future return. Before investing, agents will want to be sure that they will be able to carry out transactions with foreign residents, be it for the purchase of inputs, debt repayment, profit remittance, etc. So by removing the current obstacles, investment, future production capacity, and ultimately the expected income level of the general population is encouraged.

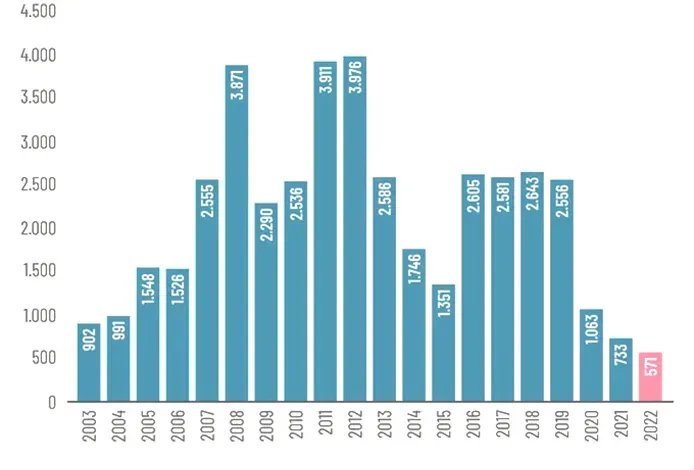

Foreign direct investment in millions of USD

Source: BCRA

On the consumption side, the elimination of exchange controls and the unification of the exchange rate would have a positive impact on expectations, which would lead to an increase in private consumption.

The reasoning behind this lies in the fact that, with an exchange control and different exchange parities, the expectation of future devaluation (which is increasing with respect to the size of the gap) will always be present and the population will seek to cover itself against the loss of capital by acquiring other assets (such as the dollar), shifting consumption to the future. Exchange rate unification, by changing expectations, could generate a consumption shock.

Is it enough to lift controls alone?

The elimination of restrictions on the official foreign exchange market is a necessary but not sufficient condition. In order to deregulate this market definitively and without this leading to an abrupt devaluation and an inflationary shock, it must be accompanied by fiscal and monetary reforms.

It could be said that monetary, fiscal and exchange rate policies are like water, flour and yeast when it comes to making bread; if we use only water and flour we will end up with grease. The three axes of economic policy must be coordinated.

Comments