We all, at some point, have kept some type of control over our money. Whether it's by recording expenses in a notebook, using an Excel spreadsheet, or through some phone application, the goal is always the same: to know how much comes in, how much goes out, and what the final result of our economic decisions is. Almost intuitively, we seek to answer a simple question: are we making or losing money?

In companies, exactly the same occurs, although with more complex and detailed tools. Before investing, producing, or expanding an activity, it is essential to know what the expected income will be and what costs will need to be incurred to obtain it. In the agricultural sector, this need becomes even more significant, as each campaign involves heavy investments, climate risks, and markets with changing prices.

To analyze these productive decisions, there is a fundamental tool called Gross Margin. It is an economic analysis methodology that allows estimating the result of an agricultural activity by comparing possible future income with the direct costs necessary to produce them. Through the economic valuation of physical variables such as yields, inputs, and products, the Gross Margin becomes a key guide to evaluate productive alternatives and make more efficient decisions within the agricultural enterprise.

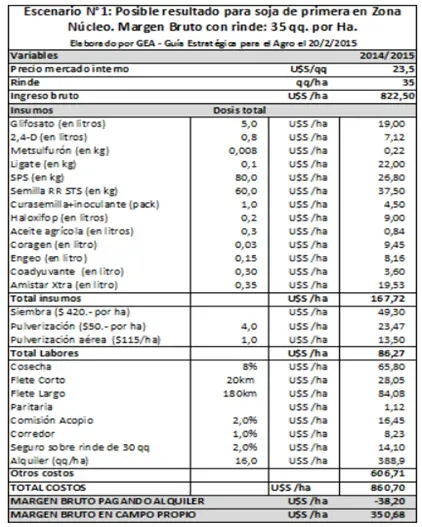

(Example of gross margin, Source: Rosario stock exchange)

As visualized, the gross margin gathers a significant amount of information relevant to the activity, such as all fixed costs, variable costs, and also provides a comparison with a reference yield and also indifference (the minimum amount of production per hectare that a producer needs to harvest to cover all production and marketing costs, without losing or making money). Therefore, the Gross Margin is not just a simple income statement applied in agriculture, but rather a Model for decision-making. Its use in agricultural decisions is due to the ease with which possible income and expenses can be estimated or calculated and the concrete possibility of changing crops from one campaign to another. In livestock companies, its use is limited due to the longer and more complex productive processes.

What is the most important point addressed by a gross margin?

It answers the common question, “What is convenient for me to produce?” It is used both as a post hoc economic control tool, that is, to analyze results already obtained, as well as a priori, allowing to project and guide future decision-making. However, both the Gross Margin per hectare and the total Gross Margin do not represent an exact measure of the real benefit of an agricultural activity, as they do not consider the total cost of the business activity. Despite this limitation, it is a quick and efficient analysis tool that helps the agricultural producer answer fundamental questions such as what to produce and how to produce, functioning as a guide to determine the most convenient activities according to productive, economic, and market conditions.

Regarding agricultural production, it is one of the most used tools. In the livestock business, the use of the gross margin presents certain limitations because these are longer and more complex production processes than in other agricultural activities. In systems such as cattle raising and rearing, the productive cycles cover several periods and require considering biological, reproductive, and management factors that develop over time. For this reason, the gross margin often fails to fully reflect the real economic dynamics of livestock activity, necessitating its complement with other indicators of economic and financial analysis.

In conclusion, the “Gross Margin” is a great decision-making tool, but for it to be a truly comprehensive tool, it should encompass Agricultural planning does not always suffice with knowing which activity leaves the highest margin per hectare. In practice, productive decisions are often conditioned by various limits, such as available capital, surface area, machinery, or even working time. Therefore, economic analysis must focus on determining which activity makes the most efficient use of the resource that is most scarce within the business.

When capital is the main constraint, the logic of analysis changes completely. In that case, it is no longer sufficient to compare only the unit gross margins, but it becomes more important to assess how much economic result each peso invested generates. This can lead to an activity that seemed less profitable in absolute terms being the most convenient option for using the limited resource better.

Under this criterion, the producer does not only seek to maximize production or margin per hectare, but to maximize the economic performance of the resource that conditions the system. Therefore, relating marginal contribution to the limiting factor becomes a key tool to decide what to produce and how to allocate the available resources as efficiently as possible.

Comments