The president and his economic team

Sources of monetary issuance

The RRII have been changing since the new president took office, but there is no doubt that the clear impact of the policies implemented to stop monetary issuance can be seen. First of all, the first source of emission from the fiscal deficit stands out, which has turned into a surplus since January of this year and remained constant until June, until there was a financial deficit in July, but the primary surplus could be maintained, which had not been achieved in the month of July for 5 years. This first source of monetary issuance is very important because, if it is possible to pay our expenses with income, the need to print banknotes disappears.

Secondly, there is the payment of interest to commercial banks; this debt has gone by many names, Leliqs, Lebacs, passive passes. Of course, these debts have generated a second source of issuance, which, although it has not been settled, a plan has been developed to eliminate these liabilities. The plan consists of the Treasury issuing bonds called Lefis, which will be delivered to the BCRA in exchange for Treasury bonds, that is, the Treasury is canceling its bonds with other bonds (Lefis). Lefis have a one-year term and have a variable monetary policy rate defined by the BCRA. Later, commercial banks use the funds they have in the BCRA's passive passes, and with that money, they buy Lefis. In conclusion, the debts pass from the BCRA to the Treasury.

Finally, the third and last source is emission through the purchase of reserves; a new policy has been adopted, which is very innovative and interesting. It consists of the BCRA buying dollars in the MULC (single market for exchanges) and injecting pesos into the economy, then going to retrieve those pesos from the parallel market (CCL, MEP). Why do this? This way, the BCRA avoids an excessive supply of money and, at the same time, can benefit from the price difference of the dollar in the different markets.

Gross International Reserves

Own preparation based on BCRA report

Regarding the chart of the evolution of the reserves, it can be noted that there was an accumulation policy under the attempt to clean up the central bank. The reserves show an increase reaching a peak in May. This could be explained by the liquidation of agricultural exports, that is, a seasonal factor. However, this growth stalled in June and July, dropping by nearly 4 billion dollars. There are several notable points of inflection where reserves increase or decrease sharply, suggesting episodes of intervention in the foreign exchange market, foreign debt payments, or speculative movements that have affected the reserves. Clearly, one of the reasons for the decline in July is the payment of interest on Bonares and global debts along with payments to the International Monetary Fund and BOPREAL. Furthermore, as Bausili explained in a press conference, reserves were used to cover seasonal energy deficits.

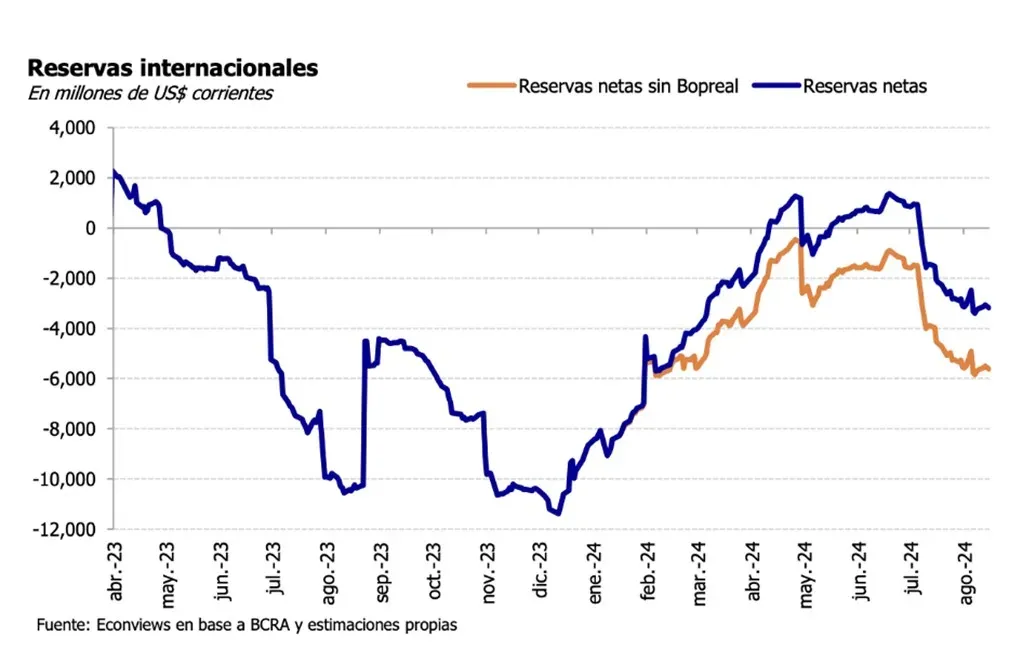

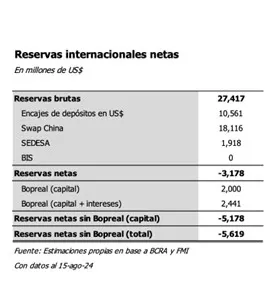

Net International Reserves

Net reserves (blue line) show a negative trend since April 2023, with a sharp drop until August 2023, reaching a low point during that period. Then a recovery is observed until May 2024, followed by another drop towards August 2024. Net reserves excluding Bopreal (orange line) remain below net reserves, indicating that without Bopreal funds, the situation of reserves is even more critical, currently reaching a negative balance of 6 billion dollars.

Comments on Monetary Policy and expectations for the future

The first critical point to highlight is the deficit of reserves. The sustained decline and negative net reserve balance suggest significant pressure on the Central Bank to maintain exchange rate and financial stability. This deficit limits the government's ability to intervene in the exchange market or meet international payments, which can increase exchange rate volatility.

Another major concern regarding the level of reserves is the dependence on the swap with China. The large proportion of gross reserves that depends on the swap with China indicates a considerable reliance on bilateral agreements to sustain reserves. This strategy could be a short-term measure to avoid a balance of payments crisis, but it is not a sustainable long-term solution without real accumulation.

Finally, the outlook for what may happen with the central bank's balance sheet in the short and long term remains uncertain. In my opinion, it is a crucial issue for the stability of the government, which will need to combine exchange rate, monetary, and fiscal policy to pay interest on the debt. Once the debts are settled, it might be possible to achieve stability with positive net international reserves, something that has not happened in the country for many years. However, it will not benefit from the boost of liquidating exports, and continuing with a negative balance will make it unlikely to reach agreements with potential organizations and investors. We will also see what can be expected regarding the reactivation of the economy. With a higher level of consumption, higher levels of revenue could be achieved, expanding the fiscal surplus. This would mean an advantage for the government since it could thus meet its debt commitments, and an increase in consumption would improve expectations, confidence, and the president's image.

References:

Comments