Since Javier Milei took office in December 2023, Argentina has experienced significant economic transformations. The current government has placed strong emphasis on macroeconomics, seeking to organize public finances and avoid spending above tax revenues. This stance represents a break from the past, as previous governments often ended their terms with large fiscal deficits and balance of payments issues. Historically, the lack of order in public accounts, regardless of political affiliation, has led to deep crises, disproportionately affecting the lower class, consumption, and production, resulting in economic recession, high inflation, and wage conflicts.

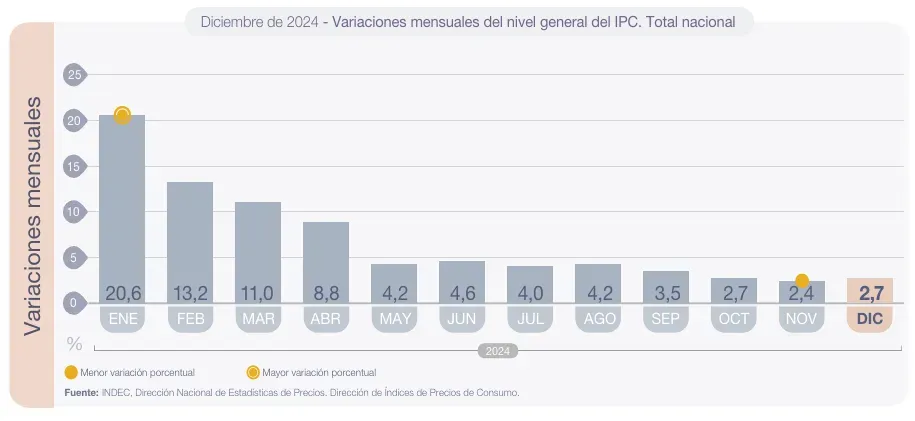

One of the first measures of Milei's government was the "sincerization" of the economy through a significant devaluation. The official exchange rate rose from approximately 400 Argentine pesos per U.S. dollar to 800 Argentine pesos, representing a 100% devaluation. This measure had a strong impact, raising prices and causing a considerable loss in the purchasing power of wages and a decrease in national production. Despite the magnitude of the devaluation, the price translation was not 100%; the inflation rate in December was approximately 25%, and in January 2024, it was 20.6%.

Throughout 2024, Argentina recorded an annual inflation rate of 117.8%. While the initial devaluation drove inflation higher in the first months, it began to progressively decline, although it has not reached the levels of a country with a stable economy.

Source: https://www.indec.gob.ar/uploads/informesdeprensa/ipc_01_2517A7124C09.pdf

Looking at the year-on-year variations of the Consumer Price Index (CPI), we can see a marked deceleration. For December 2024, the year-on-year variation was 117.8%. However, by May 2025, the year-on-year inflation had drastically dropped to 43.5%. In terms of monthly variations, inflation fell from figures close to 25% or 20% in the early months of Javier Milei's administration to 1.5% in May 2025 (the latest inflation data released by INDEC).

Source: https://www.indec.gob.ar/uploads/informesdeprensa/ipc_06_2539EA74C12F.pdf

This notable reduction in inflation is attributed by the government to the conviction that "inflation is everywhere and at all times a monetary phenomenon," a famous phrase by Milton Friedman that President Milei applies in his economic decisions. The central motto of the government is "Zero Emission."

INDEC's data seem to partly validate this perspective, but the question arises at what cost this inflation control has been achieved. Milei, an orthodox monetarist, firmly believes that inflation is a monetary phenomenon, a stance shared by many economists. However, every economic measure has consequences, which, in this case, have been borne largely by society and not by what the president calls the "political caste."

Milei's plan has been clear: to cease monetary emission and not to spend more than what is collected, seeking fiscal balance or, ideally, a surplus. This plan has proven effective in containing inflation. Nevertheless, concerns arise regarding the national economy's situation. Has economic recovery been achieved? Is the country still in recession? Has consumption increased? Are wages truly outpacing inflation, as the president claims?

Controlling inflation is an achievement of the government, but the country's economic growth is a separate issue. In the current context, it is observed that wages are strongly controlled by the national government. The government intervenes in the approval of collective bargaining agreements, and if it considers that a wage increase exceeds the expected inflation, it is unwilling to approve such an agreement. This strategy makes sense in an economic stabilization plan: to tame inflation, wages must increase below it. If collective bargaining were indexed to inflation, the stabilization plan would be ineffective, generating an upward inflationary spiral, contrary to what is sought. However, excessive wage restraint could lead to a significant decline in consumption and, consequently, production, which in turn increases unemployment and poverty.

The government has managed to order the macroeconomy, achieving fiscal surplus, increasing the Central Bank's reserves (BCRA) through IMF loans (buying dollars before having a "Flexible" exchange rate) and maintaining a "flexible" and stable exchange rate, floating within bands. This has been fundamental in keeping inflation low and controlled. The next challenge for the government is to focus on microeconomics. This implies reducing taxes, eliminating bureaucratic barriers, and a moderate opening of imports to foster greater competitiveness of national products relative to imported goods.

We are currently navigating the intermediate stage of Javier Milei's presidential management, characterized by the implementation of high-impact economic measures on the productive structure and the welfare of households. The monetarist approach adopted by the government—centered on restricting monetary emission to finance public spending—responds to a vision oriented towards macroeconomic stabilization and fiscal cleansing.

From a technical and/or academic perspective, the systematic use of monetary policy to address budgetary imbalances can generate positive externalities in the short term, such as stimulating aggregate demand through increased spending (GDP = C + I + G + (X – M)). However, the effects in the medium and long term are particularly relevant: financing through emission tends to erode price stability, distort incentives in markets, and compromise the saving and investment capacity of economic agents (citizens). Inflation, as a cumulative and persistent phenomenon, negatively impacts the purchasing power of wages and generates uncertainty in consumption and investment decisions.

The current fiscal strategy seeks to correct these imbalances through a budget adjustment that prioritizes spending efficiency and reducing the primary deficit. Nevertheless, structural challenges remain that must be addressed with social sensitivity and technical prudence: labor informality, the regressiveness of certain taxes, and the limited capacity of the State to generate counter-cyclical policies without compromising financial sustainability.

While the adopted course offers encouraging signs of macroeconomic correction, the design of complementary measures will be key to mitigating the distributional costs of the adjustment. The decisions made during this stage will be decisive in consolidating a path of balanced, inclusive, and sustainable growth.

Comments