Today I want to talk about one of my portfolio companies: Nubank, the neobank that has rewritten the rules of banking in Latin America and now has its sights set on the world. In just a few minutes, I will tell you how a simple idea born out of frustration became a financial phenomenon that is redefining what it means to be a bank in the 21st century.

A Revolutionary Beginning: Frustration as a Driver

Picture this: it's 2012 in São Paulo. David Velez, a partner at Sequoia Capital, is fed up with the banking bureaucracy, endless lines and abusive fees of traditional Brazilian banks. The straw that broke the camel's back was not being able to open a basic account after hours of trying. So, out of that personal frustration, a simple but powerful question was born: What if we created a bank with no branches, no paperwork and no fees?

From this idea came Nubank in 2013, and with it, the iconic purple credit card, the "roxinho". It was not just a card; it was a symbol of rebellion against an obsolete system and the beginning of customer-centric digital banking.

The Formula for Success: Customer, Data and Scale

Nubank's initial strategy was simple: a credit card with no fees, transparent terms and an exceptional mobile experience.

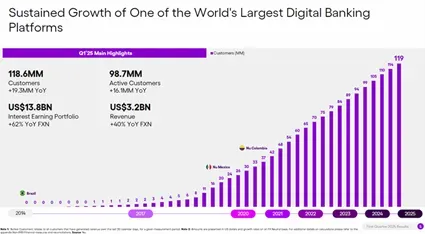

But underneath that simplicity was a sophisticated model. Every satisfied customer became an evangelist, driving massive organic growth. By 2016, they had over a million customers with minimal marketing spend. Their Net Promoter Score (NPS), a measure of customer satisfaction, exceeded 85, unheard of in the financial sector.

This obsessive focus on the customer not only generated loyalty, but also allowed them to expand beyond credit cards, adding savings accounts, checking accounts and adopting Brazil's popular instant payment system, Pix. By the first quarter of 2025, Nubank already had more than 100 million customers in Brazil alone, with approximately 60% considering it their primary bank.

Thanks to this model, Nubank achieved efficiency metrics that make traditional banks pale in comparison: an average monthly cost per active customer of only $0.70 and an efficiency ratio of 24.7%, well below the 50% of its competitors.

Latin American Expansion: Lessons Learned

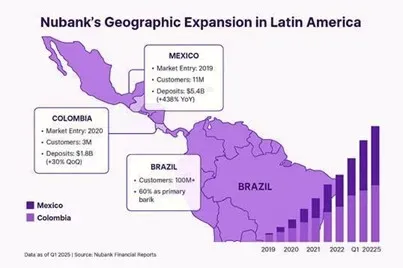

With the success in Brazil, expansion into Mexico (2019) and Colombia (2020) was the next logical step. These markets shared similar challenges: concentrated banking sectors and an underserved population. However, the expansion was not a simple copy-and-paste. Nubank adapted its products to local needs, while maintaining its digital approach, no commissions and exceptional customer experience.

The results are impressive: 11 million customers in Mexico and nearly 3 million in Colombia by the first quarter of 2025. In Mexico, its deposit base grew by a staggering 438% year-on-year. In addition, the recent approval of their banking license in Mexico in April 2025 is a crucial milestone, as it will allow them to further expand their product offering and consolidate their position. This geographic diversification not only increases their revenues, but also reduces their dependence on a single market.

Beyond Banking: The Nubank Ecosystem

What really sets Nubank apart is its ambition to go beyond traditional banking services. What CEO David Velez calls "Act 2" of their strategy is building a comprehensive financial ecosystem. They have launched initiatives such as NuCel (a mobile operator), NuTravel (a travel platform), a NuMarketplace and NuPay (a payments solution for merchants).

At first glance, these may appear to be disconnected moves, but they have a strategic logic. By offering services such as telecommunications or travel, Nubank increases customer touch points, generates valuable data on their consumption habits and diversifies its revenue streams beyond traditional interest and bank fees. This creates an ever-deepening competitive "moat", making it very difficult for other players to match its offering.

Global Ambitions: Act 3

Nubank's "Act 3" is the boldest vision: global expansion. Although it's still early days, the company is already laying the groundwork. They are investing heavily in high-density AI data centers and developing modular systems that can adapt to diverse regulations and financial cultures. The hiring of Roberto Campos Neto, former president of the Central Bank of Brazil and an internationally respected figure, is a clear sign of their seriousness in this area.

The challenge is enormous, as banking is highly regulated at the national level. However, Nubank's methodical approach, building a solid foundation before launching into new markets, is a promising sign. They are not looking for opportunistic expansion, but for sustainable global growth.

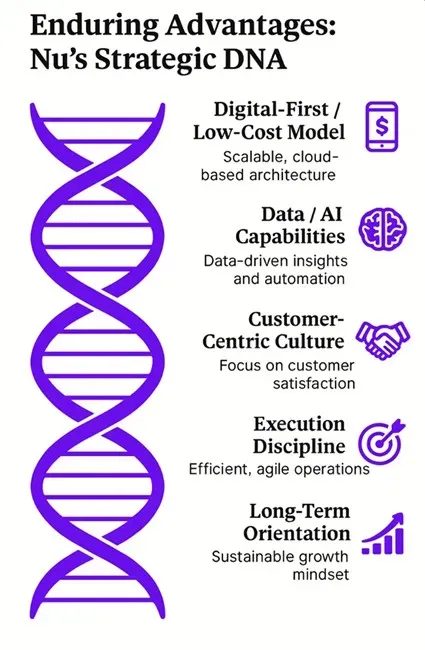

Nubank's DNA: Unbreakable Advantages

So what are the keys to their success? The low-cost model allows them to offer low fees and better rates. Their data advantage and aggressive investment in AI allow them to make better credit decisions and personalize services. And their customer-centric culture ensures that strategic decisions always prioritize the long-term relationship.

These advantages are mutually reinforcing: lower costs attract more customers, which generates more data, which improves risk management and profitability, funding the expansion of the ecosystem. It's a virtuous circle that grows stronger with scale.

The Purple Road to the Future

What started as a personal frustration for David Velez has transformed into a true financial revolution. Nubank's "Purple Road" is not just a marketing slogan, but a distinctive strategic philosophy that has proven remarkably effective. With returns on equity approaching 30% and revenue growth of 40% year-on-year, Nubank is proving that it is possible to be profitable while building trust and serving millions of previously underserved people.

Nubank's future promises to remain exciting. We will be watching its evolution in Mexico, the performance of its new verticals and, of course, the progress of its global ambitions. Undoubtedly, its journey is just beginning.

Comments