• Important clarification: this note was originally published on July 26 of this year, but due to a technical issue, it had to be re-uploaded. Therefore, this article does NOT contain data from the last 2 months; all data are prior to the original publication date.

• If you want to see current market data about Bitcoin and Ethereum, I leave you the last 2 notes I published about them analyzing various areas ↓

- Bitcoin: What differences do the indicators show between 2021 and 2025?

- Ethereum: What differences do the indicators show between 2021 and 2025?

Beginning of the original note:

A) First federal pro-crypto laws in the U.S.

B) The institutional evolution of Bitcoin and Ethereum.

C) Ethereum and its ecosystem.

D) The Wall Street narrative.

A) First federal pro-crypto laws in the U.S.

First of all, it is important to point out that this year the Republican Party came to power in the U.S., which demonstrated its solid support for the cryptocurrency sector during the 2024 presidential campaigns, to the extent that they published on their official page: “Republicans will end the illegal and anti-American offensive against cryptocurrencies by the Democrats and will oppose the creation of a central bank digital currency.” Even Trump declared: “I will ensure that the future of cryptocurrencies and Bitcoin is made in the U.S.,” “We want all remaining Bitcoins to be printed in the United States!” and “Our country must be a leader in this field. There is no second place!.” Currently, they are gradually fulfilling their campaign promises, among them, they created a strategic Bitcoin reserve for the country and are building a regulatory friendly environment for the sector. One of the most relevant aspects is that the CLARITY Act (Digital Asset Market Clarity Act) is currently being processed; this is the first comprehensive federal law for digital assets in the U.S.

It aims to end the regulatory mess surrounding cryptocurrencies in the United States, providing them with a pro-crypto framework. The law has bipartisan support, but with a wide Republican majority, almost 100% of Republicans and about 40% of Democrats voted in favor in the House of Representatives (the preliminary step to the Senate).

Regarding what has been mentioned, it is important to note that, in the past, the Biden administration attacked this sector, which caused the regulatory risk to be very high, preventing large-scale institutional investments in this market. This new regulatory certainty eliminates that risk, which is why it is so relevant in the medium to long term. Projects will know exactly what requirements they must meet and institutional investors will be able to operate with clear and permanent rules. Overall, the regulation will provide legal security to the entire ecosystem.

One of the most relevant points addressed by the law is that not all these assets will be grouped under the same legal concept, but rather classified into two: 1) Digital Commodities: Truly decentralized and autonomous cryptos like Bitcoin and Ethereum, and 2) Digital Securities (Digital Asset Securities): Tokens whose evolution depends on the work of a centralized company or promoter. It will also define a transparent and rigorous process for any other cryptocurrency (for example, Solana or XRP) to be able to become a Digital Commodity, as long as it meets the required technical standards. To better understand what has been mentioned, keep in mind that currently gold and silver are considered Commodities, meaning that truly decentralized blockchains (BTC and ETH initially only) would be part of the same concept to which precious metals belong.

Also, for the first time in history, banks and financial companies in the U.S. will be allowed to operate with cryptocurrencies as part of their normal financial activities, allowing them to offer services such as custody, trading, and loans linked to these digital assets. This regulatory opening facilitates the entry of traditional institutions to the crypto market, increasing liquidity and stability, and significantly boosting institutional adoption.

Tim Scott, Chairman of the Senate Committee on Banking, Housing, and Urban Affairs, anticipated that the law would be voted on by the Senate by the end of September.

Additionally, there are two other relevant pro-crypto laws: GENIUS and Anti-CBDC. The first revolves around regulations favoring stablecoins, such as crypto dollars like USDT or USDC. This has already been approved by both Chambers and signed by Trump. On the other hand, Anti-CBDC focuses on prohibiting the creation of a digital currency issued by the U.S. Government. This has just passed to the Senate as CLARITY.

The three laws, together with internal regulations from the SEC and CFTC, will form the new pro-crypto regulatory core in the United States, establishing a clear, competitive, and prosperous legal framework for the coming years.

B) The institutional evolution of Bitcoin and Ethereum.

Last year, despite the fact that the Democrats were still in power, the largest investment funds in the world, such as Blackrock and Fidelity, managed to have Bitcoin and Ethereum start trading on Wall Street through financial instruments called ETFs. Thanks to this, for the first time, these cryptos could be bought on the stock exchange, just like buying shares of Apple. This opened the doors for both assets to receive new institutional demand that they previously lacked since they could only be purchased on exchanges (cryptocurrency banks like Binance) or privately. Let's delve deeper into each case.

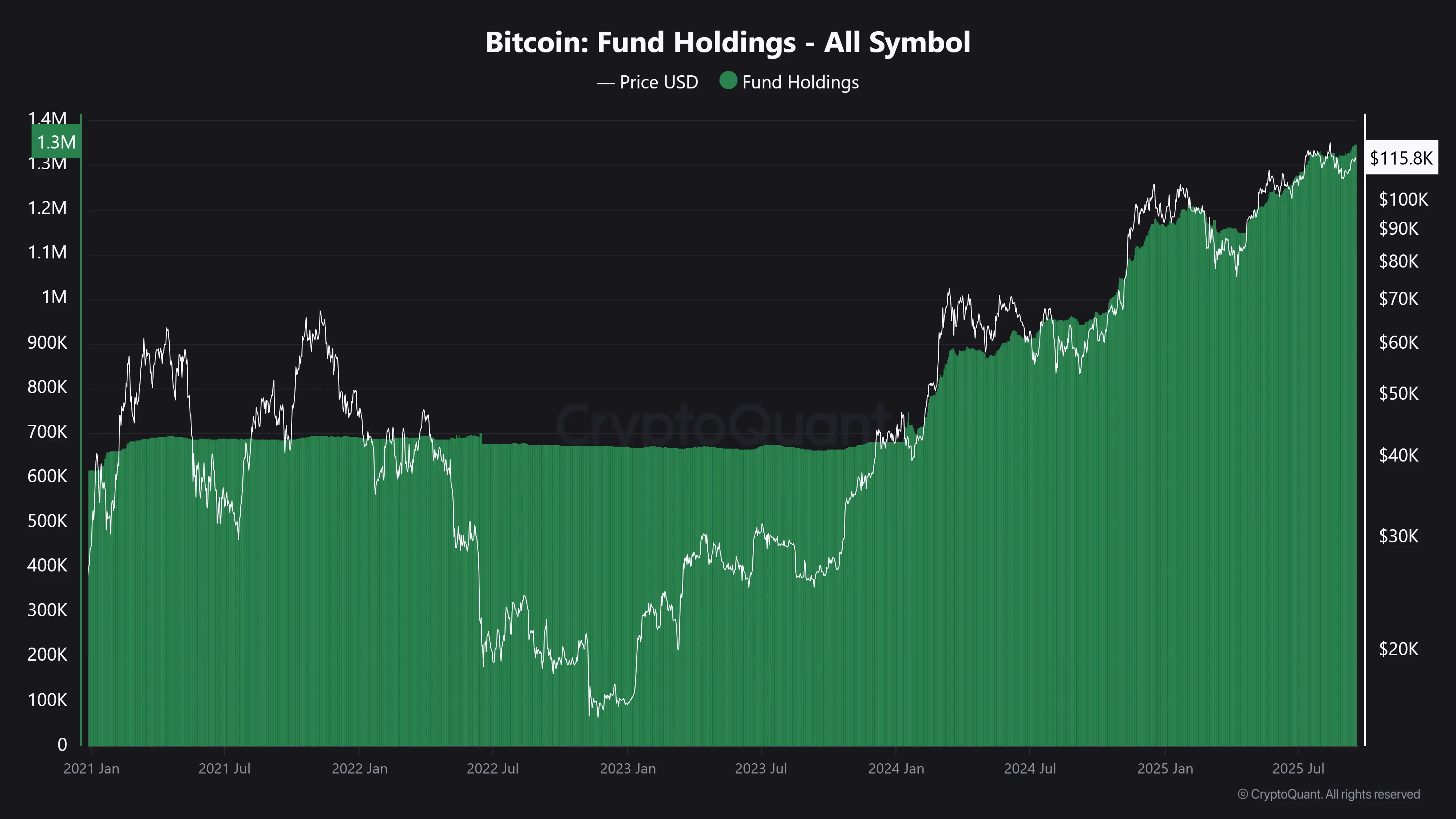

1) Bitcoin.

This accompanying chart represents the price of Bitcoin (white line) vs the amount of BTC purchased by investment funds (green area).

As you can see regarding the green area, from 2021 to 2024 it remained completely flat, without demand, but after BTC started trading on Wall Street, it began to increase constantly along with its price. There are several triggers that caused the increase in Bitcoin's value, and one of the most important is this.

Investment funds like Blackrock (the one that manages the most money worldwide) began to explain to their clients what Bitcoin is and how it works, that is, they educated their investor community, primarily transmitting that it is the new digital gold. This caused BTC to conceptually evolve in the eyes of institutional investors from being an internet users' cryptocurrency to a long-term store of value.

The CEO of BlackRock, Larry Fink, made statements such as: “Bitcoin is digital gold,” “Bitcoin is legitimate, it is a legitimate financial instrument,” and “Tokens are the next generation for markets.”

As of July 18, 2025, Wall Street investment funds hold 1,317,000 Bitcoins, which is approximately 7% of all circulating BTC. The price of BTC at the time of writing this note is approximately 120,000, making this amount represent 158 billion USD. Besides this total absorbed by Wall Street, there are also Bitcoin treasuries held by governments and companies totaling 1,400,000 BTC (168 billion USD).

If you want to delve into Bitcoin and its ETFs, I recommend reading the latest note I wrote on the subject, on October 15, 2023, before Bitcoin actually reaches Wall Street. The price of Bitcoin at that time was 27,000 USD:

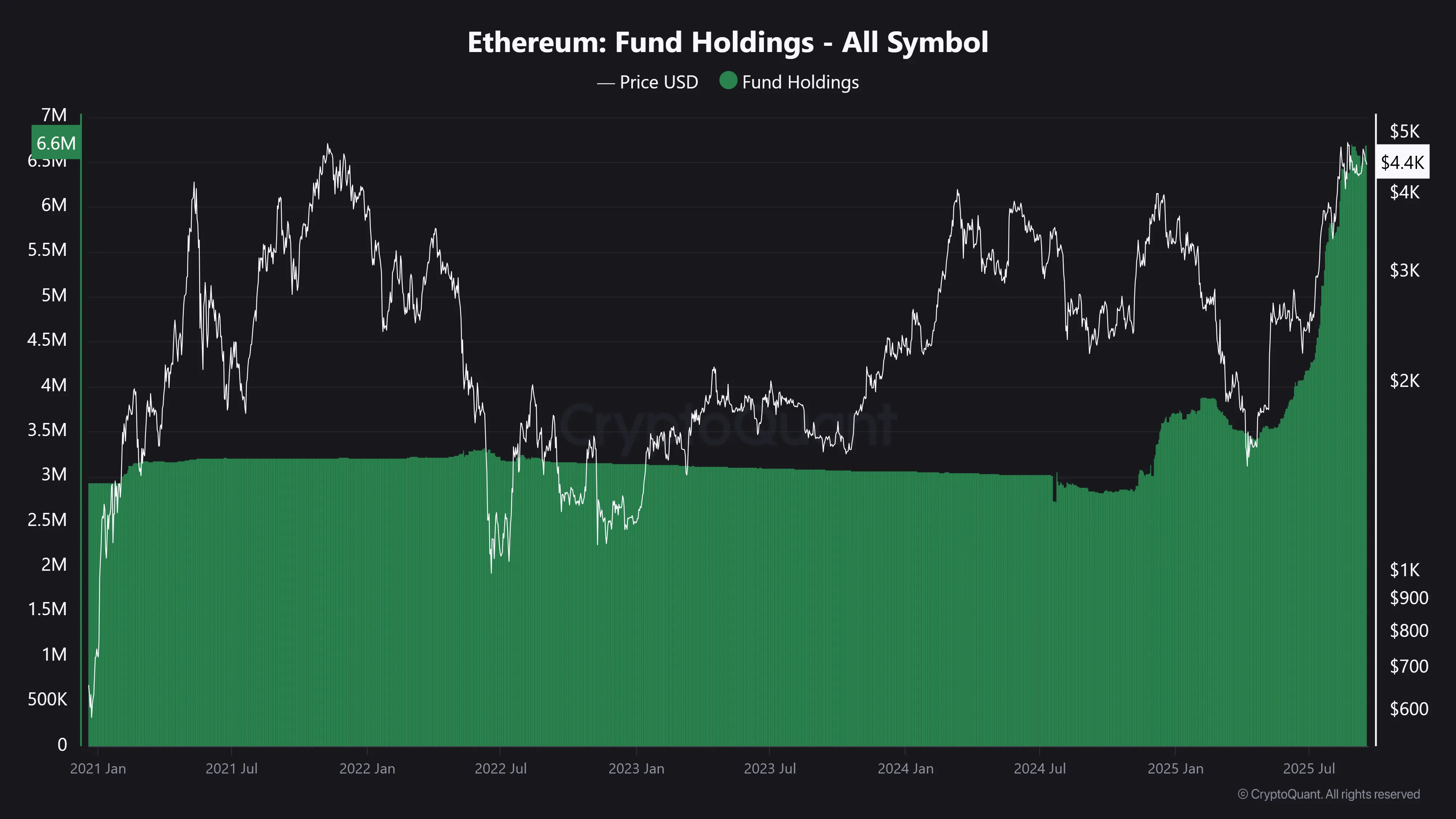

2) Ethereum.

ETH is a very different case from BTC. They are not the same, nor are they programmed the same way. But beyond their significant technological differences, I want to focus on their differences in the eyes of institutional investors: Bitcoin is digital gold and Ethereum is going to be a digital bond.

This distinction arises because Ethereum has something that Bitcoin does not: staking. Through this, annual returns can be generated in ETH, that is, it functions like a fixed-term deposit in pesos, but in ETH. You deposit your Ethereum in staking, and that gives you the possibility to access an annual return in the same cryptocurrency. This way, you can generate profits without needing to sell the original stock. This is truly profitable if you are operating with large amounts like institutional investors, as the annual return is 3-4% in ETH (not in USD).

Why did I write “is going to be” and not “is”? Because although ETH began trading on Wall Street in July 2024, the attack from the Democratic Party on the crypto sector continued in that context, leading the SEC (the agency that regulates ETFs on Wall Street) to consider the staking service as a possible UNregistered security, causing the ETF containing this service to perhaps not be approved. Issuers preferred to sacrifice the return to obtain the green light. All managers, from BlackRock to Fidelity, removed the staking clause from their forms and managed to have the SEC authorize listings quickly, but without this service, which is the key differentiator between Bitcoin and Ethereum.

Everything changed since the Republican Party won the elections in November 2024. Here I accompany the same chart as before, but for ETH. The white line represents its price, and the green area represents the amount of ETH purchased by investment funds.

As you can observe regarding the green area, from 2021 to November 2024, it remained completely flat, without demand, but after Trump won the elections, the demand for ETH began to increase. The election of the Republican Party represented a future friendly regulation towards cryptocurrencies.

Only in May of this year did the SEC, now composed of pro-crypto officials due to the change in government, recognize staking on PoS blockchain networks (e.g., Ethereum) as an activity NOT subject to securities registration, removing the main legal obstacle for custodians, brokers, and Wall Street ETFs to be able to offer ETH returns to their clients.

Although this has been generally authorized, the staking service in the ETFs that trade on the stock exchange still needs to be specifically approved. The next deadline for the SEC to authorize this is at the end of October, and it is estimated that they are first waiting for the CLARITY Act to come into effect.

This new regulation also impacted institutional demand; the graph shows how starting in May, the green area (ETH purchased by funds) increased. Moreover, only now, in mid-July, did its ETF have a record of weekly purchases through Wall Street; in just one week, more than 2.1 billion USD were purchased.

Specifically, as of July 18, 2025, Wall Street investment funds hold 4,991,000 ETH, which is approximately 4% of all circulating ETH. The price of Ethereum at the time of writing this note is 3,500 USD, making this amount represent 17.5 billion USD.

Besides this total absorbed by Wall Street, there are also private companies that have created ETH treasuries to start offering this service, but through their shares. That is, you buy shares of a company that mainly possesses an ETH treasury, and with that, you can be part of the annual interests generated through staking. While this has a very relevant impact, what is truly awaited is for the ETFs from the largest investment funds in the world, like Blackrock, to provide this service to their clients. Between corporate treasuries and other strategic entities, a total of 1,700,000 ETH has already been purchased separately, which is 6 billion USD.

The staking service for now would be only for Ethereum, but there are other cryptocurrencies, less established and higher risk, that also have this system, so it is very likely that in the near future there will be other crypto ETFs trading on Wall Street with staking.

Regarding the ETH ETFs, BlackRock believes they were successful but are still incomplete due to the inability to provide this service. Robbie Mitchnick, the Director of Digital Assets at the company, said: “The inability to earn income through staking via this product may be a significant factor that hinders its growth. He also clarified: "An Ethereum ETF without staking functionality is incomplete", and explained that "The income from staking is an important part of generating additional revenue". Additionally, the company met with the new SEC, now composed of pro-crypto officials, to discuss everything related to staking and They argued that including staking performance in their ETH ETF would significantly improve the product..

Despite everything mentioned, in March of this year, BlackRock's ETH ETF (ETHA) became the third fastest in Wall Street history to reach 10 billion USD in assets.

In this sense, for now, only Bitcoin has seen overwhelming demand through Wall Street, while Ethereum is just beginning. It is important to highlight that this new type of demand that has entered the crypto market is very relevant, as a new influx of liquidity to these assets allows them to become more solid and gain institutional validity. For example, Bitcoin this year was the cryptocurrency that withstood the historic international financial crisis caused by Trump's tariffs, and Ethereum is among the cryptocurrencies that recovered the fastest after the major crash.

C) Ethereum and its ecosystem.

It is important to point out that decentralized blockchain assets like ETH are more than just a chart; there are dozens of indicators to evaluate and analyze them, from on-chain metrics, derivatives, liquidity flows, etc. Therefore, before investing in any of these assets, it's crucial to first learn about blockchain technology, correctly select and interpret the indicators, and stay updated on macroeconomic, regulatory news, etc.

Furthermore, it is not the same to analyze the token of a centralized company that holds private information as it is to analyze a decentralized cryptocurrency with all of its data being 100% public. Blockchains bring this benefit: pure transparency, which allows for auditing at any time; this is called on-chain data.

Now, I will focus specifically on three indicators, but before diving into each one, I will provide a bullet point of how much money each point represents. At the time of writing this note, the price of ETH is 3,500 USD:

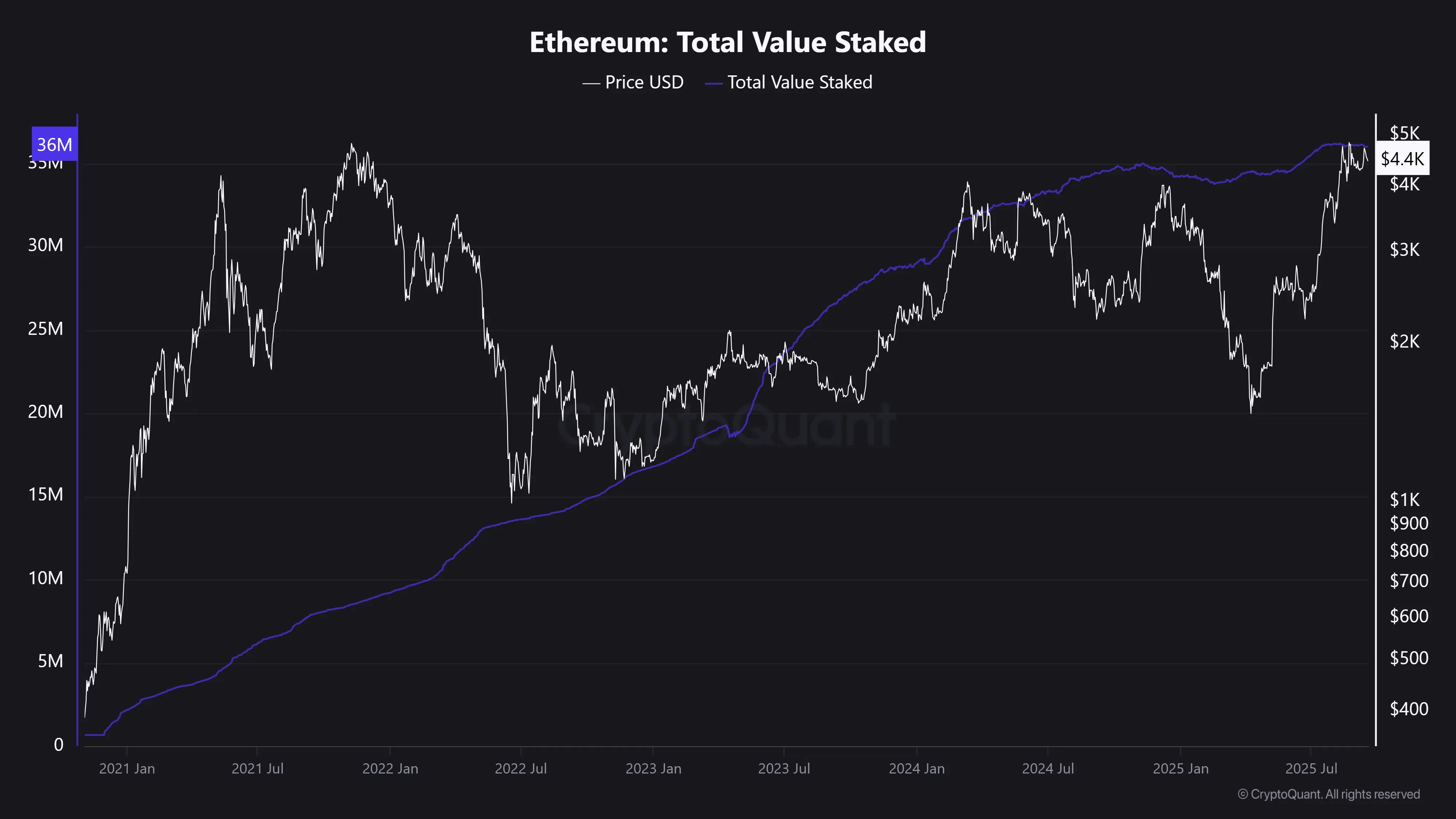

1) Total value staked: 126 billion USD (36 million ETH).

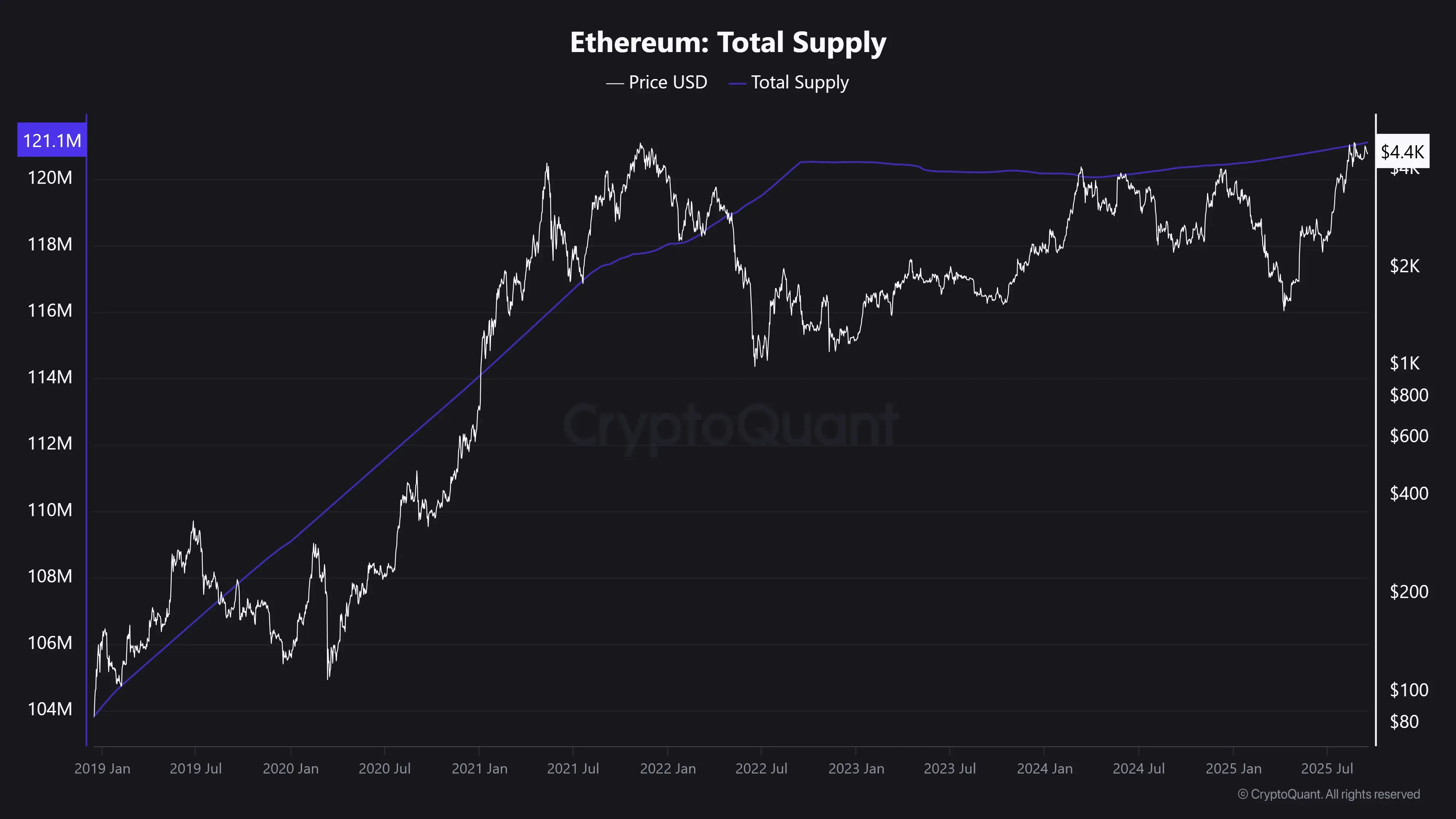

2) Total supply: 420 billion USD (120 million ETH).

3) TVL DeFi: 80 billion USD.

1) Total value staked: Amount of ETH deposited in staking generating interest.

In this chart, the purple line represents the amount of ETH deposited in staking and the white line is the price of ETH.

It can be observed in the graph how over the last four years, the amount of ETH deposited in staking generating interest has not stopped increasing, regardless of what price it is or what's happening in the world. This is very positive as it reflects a solid and constantly evolving ecosystem.

As of July 18, 2025, there are 36 million ETH (30% of the total supply) deposited in staking (as of now, Wall Street is not part of this; staking for ETFs would be authorized by the end of October), representing 126 billion USD.

2) Total supply: Amount of ETH in circulation.

In this chart, the purple line represents the amount of ETH in circulation and the white line is the price of ETH.

As you can see, until 2022, the purple line kept increasing; this was because the issuance of ETH was initially unregulated and its inflation was very high. However, after that year, the consensus protocol was updated, leading to a nearly flat inflation rate. The chart shows how the issuance from 2022 has flattened (purple line) and ceased to increase vertically.

The annual inflation of Ethereum is not fixed; it is variable. If there is a high usage of the network, it can even be negative and deflationary due to the burning of ETH. This gives it an annual margin of approximately 0.5-0.7% inflation, which, when compensated by the demand the asset has from Wall Street, its staking, etc., is imperceptible.

As of July 18, 2025, there are 120 million ETH in existence (30% of which, i.e., 36 million, are deposited in staking). This means that the total market capitalization of ETH is 420 billion USD.

3) TVL DeFi: Amount of money locked in the Ethereum blockchain.

Regarding this point, it should be clarified that the financial market of blockchain technology is much more than Bitcoin; it all started with it, but it is a First Generation blockchain. Currently, this technology has evolved, and there are new cryptocurrencies from Second Generation blockchains where applications for usage exist and can be programmed.

The first and most important Second Generation blockchain is Ethereum. There is a massive ecosystem functioning on its blockchain, and millions of transfers occur daily.

The most significant invention that came with it was the creation of: DeFi (decentralized finance). This is a system of applications for anyone to lend, take loans, exchange, or earn interest peer-to-peer without banks or intermediaries. Everything is executed automatically on the Ethereum blockchain, and anyone with internet access can participate.

Currently, as seen in the indicator, the amount of money locked in ETH's decentralized finances is 80 billion USD. This is separate from the 126 billion USD (36 million ETH) that are in staking. In total, more than 200 billion USD are part of the ecosystem created by Ethereum.

D) The Wall Street narrative.

Everything observed in this note demonstrates how the cryptocurrency ecosystem is in full growth and is shifting from being just internet user assets to institutional assets that are listed on Wall Street. If the deadlines for October are met, we should see the pro-crypto agenda of the U.S. already in motion.

Furthermore, this year, following the major tariff crisis, the importance of having an asset with institutional demand became evident, the risk-reward ratio is more balanced. The rules have changed since this market stepped into the U.S. stock exchange, and this was strongly felt with the temporary financial crash caused by the tariffs. Buying cryptocurrencies that only depend on demand coming in through exchanges (cryptocurrency banks like Binance), can be very risky. Personally, I will only focus on those cryptos that already have demand through Wall Street (BTC and ETH) and I will consider adding others that are about to be listed there (for example: XRP or SOL). Beyond my personal opinion, I repeat what was said earlier, before investing in this market, consider that: decentralized blockchain assets like Ethereum or Bitcoin are more than just a chart; there are dozens of indicators to evaluate and analyze them, from on-chain metrics, derivatives, liquidity flows, etc. Therefore, before investing in any of these assets, it is essential to first learn about blockchain technology, correctly select and interpret the indicators, and stay updated on macroeconomic, regulatory news, etc.

Finally, I emphasize that each reader must decide whether it is worth investing in Bitcoin or other assets in the short, medium, or long term, should they consider them undervalued. What is presented here is not an investment recommendation; each person must conduct their own research and arrive at their own conclusions. Always invest prudently, with buying and selling strategies. Investments here are very volatile and high-risk, especially for new users who are prone to falling for scams or thefts or buying at new all-time price highs and then selling during a significant correction, causing them extensive losses for not being aware of market cycles.

The worst mistake one can make in this market is to be impatient and let themselves be carried away by greed or panic.

Comments