Where are we?

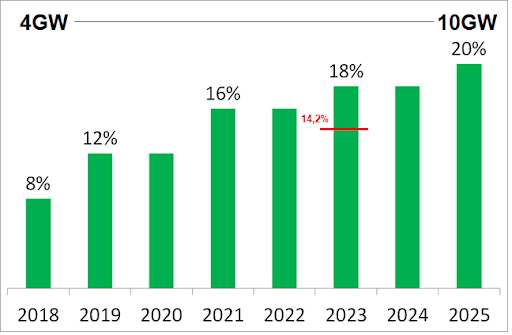

Currently, the penetration of renewable energies ( wind, solar, mini hydro, biomass/biogas) is 2Q 2023 in 14.2% of the total electricity demand. Far from the 18% stipulated in Law 27191 (EERR) and without clear perspectives on how to achieve the targets from 20% to 2025

Renewable active power: 4,716 MW and the most contributing electric regions are Patagonia, then Buenos Aires and NOA. The maximum instant penetration was 29.7%, without generating network disturbances. Although we know its advantages (almost infinite resource, almost zero emissions, competitive costs), renewable energies have 3 cons: they are intermittent (it is produced when the resource is available), they are not desecrated (whether it is used or desecrated) and generation forecasts are uncertain (depending on weather forecasts).

With the exception of some cases, most generators are national flag (main: Genneia, 360E, Pampa, YPFL, PCR, CP). It is an intensive sector in the use of capital and the generators used a lot of forms of financing: Project finance, Corporate finance, equity itself, green obligations, etc...The current installed wind power is 3.404 MW (61 generators) and will incorporate other +262MW in the end of the year. The average FC is 50%, which allows to ensure an average generation of 1400 MW /1700 MWFor its part, solar energy has an installed power of 1,311 MW (49 generators) and is planned to incorporate other +37 MW to the system. The average FC are 28-30% and the average generation is 250-400MW.Renewable energy sources (i.e. waste energy) are 1 to 4%, depending on seasonality.Where are we going?

EERR purchase contests are not planned for the system. However, there is a sustained demand of large/median private users via the MATER channel, where a private purchases a generator and transits through the network (which charges a toll).The main restrictions are: access to currencies for the payment of imported equipment and the lack of power transmission capacity.The SE has awarded new renewable energy contracts to replace forced fossil generation at certain points in the country (NOE/Litoral) with a total of 635 MW. The projects will be built between 3Q 2023 and end 2024.In addition, the SE published a new thermal contest ( Res621/23) by 3000 MW, aimed at repotentiating existing capacities or building new plants.Finally, the Mater 360 was launched to incorporate up to 130 MW into the Central corridor – Cuyo – Northwest Argentino (NOA) and up to 400 MW for export in Missions – NEA – Litoral. It also introduces the novelty of referential A, which allows to present projects that have only ensured a 92% injection capacity (about 800 MW)Still, we are far from fulfilling the goals of renewable energy. The market seems receptive to generating greater demand, the generators are willing to invest, the key goes through the execution schedule (and financing) of electrical transportation infrastructure.What innovations will be introduced?

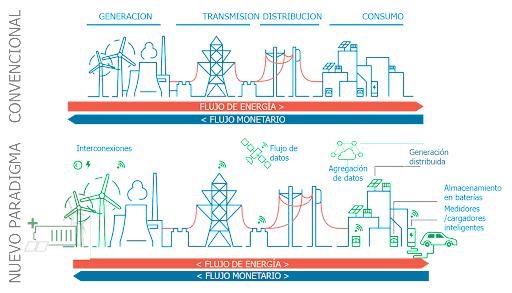

The energy sector plays a key role in the energy transition. Let us mention some changes that are experiencing:- New paradigm in monetary and energy flows: electrical systems interconnections, digital asset management, distributed generation protagonism (prosumers), energy storage emergency in batteries, etc. .

- Battery power storage systems (LFP4 or lithium mainly)

- Continuous improvements in wind and solar generation technologies that allow pending cost maintenance

- Emergency of electromobility (which may have exponential evolution)

- Green hydrogen as an energy vector of the future (not competitive today, but an international market emerges)

- Hybrid solutions SOL+BATERIAS+TÉRMICO for sectors with specific needs such as Litio/Cobra mining (off-grid/Extreme conditions)

Comments